Usda Loan El Paso

The USDA Rural Housing Mortgage Lender program is a great opportunity for individuals and families who are looking to purchase a home in rural areas. This program is designed to help low to moderate-income households achieve their dream of homeownership. Whether you are a first-time homebuyer or looking to refinance your current mortgage, the USDA Rural Housing Mortgage Lender program is worth considering.

The Difference Between USDA Rural Housing Mortgage Lender 502

The USDA Rural Housing Mortgage Lender 502 program is a type of loan designed for low-income households in rural areas. This program offers flexible credit requirements and low-interest rates, making it an attractive option for those who meet the eligibility criteria. The 502 program can be used to purchase existing homes, new construction, or to make repairs and renovations to an existing home.

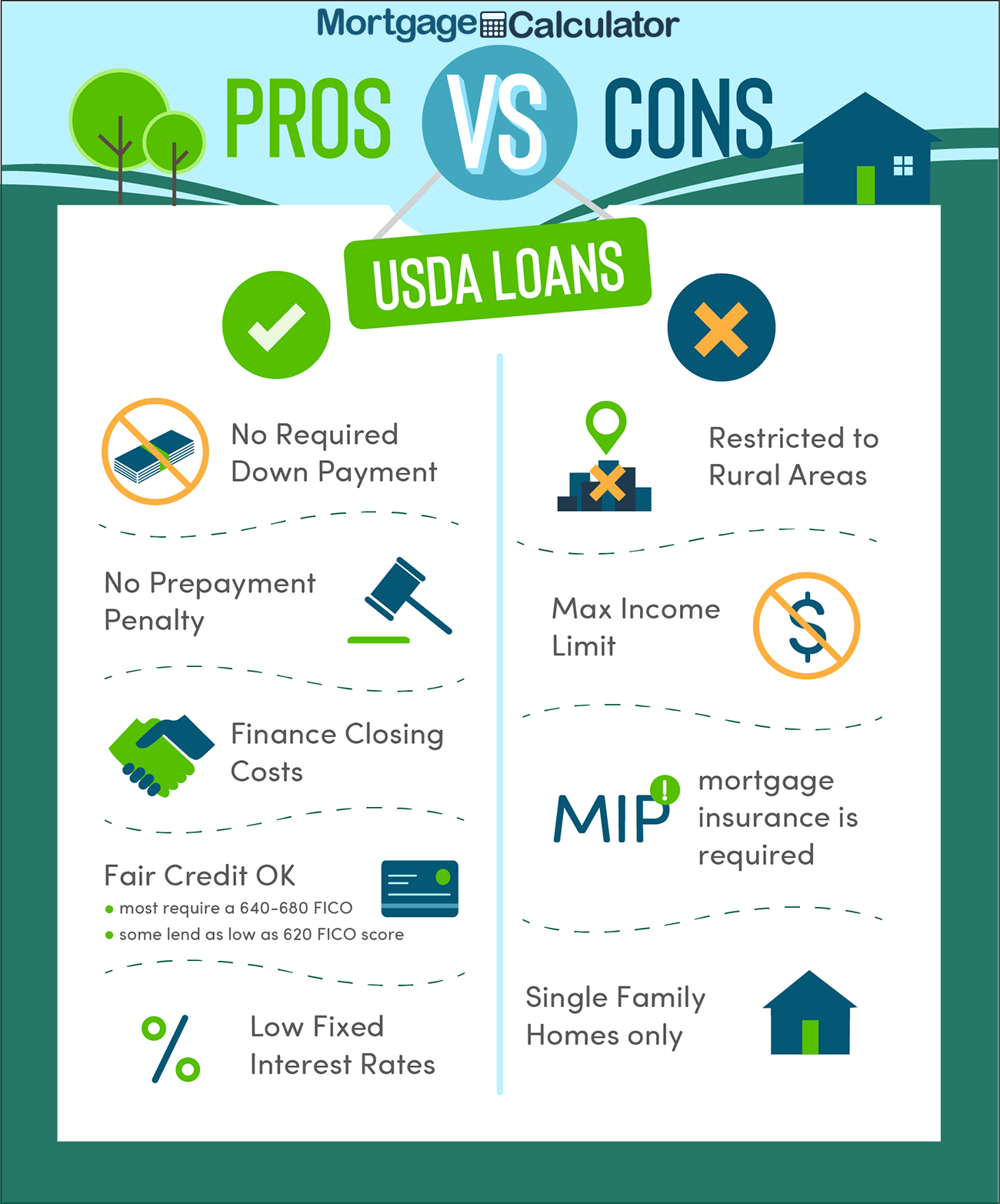

One of the key benefits of the USDA Rural Housing Mortgage Lender 502 program is that it does not require a down payment. This means that borrowers can purchase a home without having to save up a large amount of money for a down payment. Additionally, the program offers 100% financing, which means that borrowers can finance the entire purchase price of the home, including closing costs and any necessary repairs or renovations.

USDA Loan Guidelines and Requirements

In order to be eligible for the USDA Rural Housing Mortgage Lender program, applicants must meet certain guidelines and requirements. First and foremost, the property being purchased must be located in a designated rural area. The USDA provides a map on their website that can help individuals determine if a particular property is in an eligible area.

Additionally, applicants must meet certain income requirements. The USDA Rural Housing Mortgage Lender program is designed to help low to moderate-income households achieve homeownership, so there are income limits in place to ensure that the program is going to those who need it most. The income limits vary by location and household size, so applicants should check with their lender or the USDA to determine if they meet the income requirements for their area.

Other requirements for the USDA Rural Housing Mortgage Lender program include having a credit score of at least 640 (although some lenders may have different requirements), being a legal resident of the United States, and having a stable income and employment history.

The Benefits of the USDA Rural Housing Mortgage Lender Program

There are many benefits to the USDA Rural Housing Mortgage Lender program, including:

- No down payment required

- 100% financing available

- Flexible credit requirements

- Low-interest rates

- No limit on seller contributions or gifted funds

Additionally, the program allows for a wide range of property types, including single-family homes, townhomes, and condominiums. This means that borrowers have more options when it comes to finding the perfect home.

Another benefit of the USDA Rural Housing Mortgage Lender program is that it allows for financing of repairs and renovations. This means that borrowers can finance the cost of necessary repairs or renovations, which can be especially helpful for those purchasing an older home that may require some updates or repairs.

The Drawbacks of the USDA Rural Housing Mortgage Lender Program

While there are many benefits to the USDA Rural Housing Mortgage Lender program, there are also some drawbacks that borrowers should be aware of.

First, the program is only available for homes located in designated rural areas. This means that individuals who want to purchase a home in a more urban or suburban area may not be eligible for the program.

Additionally, the income requirements for the program may be too restrictive for some borrowers. The program is designed for low to moderate-income households, which means that those with higher incomes may not be eligible for the program.

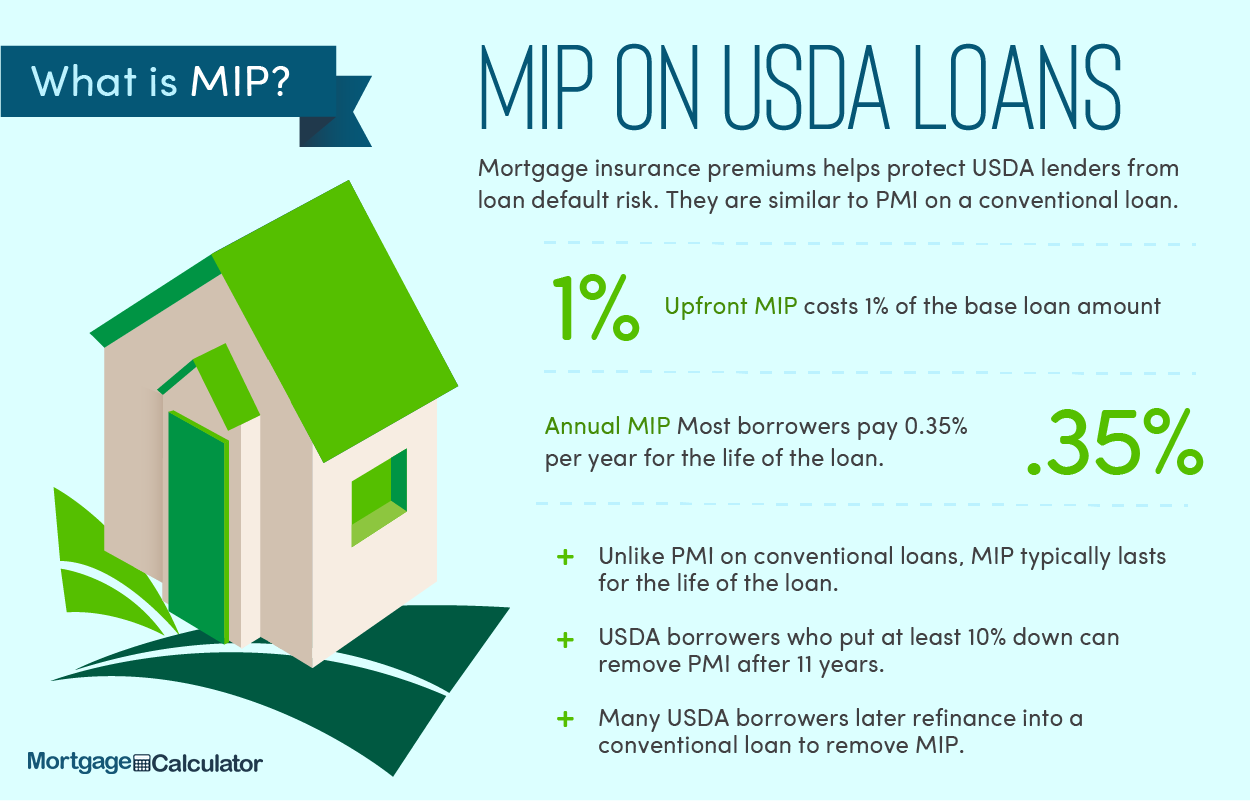

Finally, the program requires borrowers to pay mortgage insurance, which can add to the overall cost of the loan. The mortgage insurance is typically higher than what borrowers would pay for traditional mortgage insurance, which means that borrowers should factor this additional cost into their budget.

The Application Process for the USDA Rural Housing Mortgage Lender Program

The application process for the USDA Rural Housing Mortgage Lender program is similar to that of other mortgage programs. First, borrowers must find a lender that is approved to offer the program. This can typically be done by searching online or by asking a real estate agent for recommendations.

Once a lender has been chosen, borrowers will need to complete a loan application and provide documentation such as income and employment verification, tax returns, and bank statements. The lender will also need to verify that the property being purchased meets the USDA's guidelines for eligibility.

Once the loan application has been submitted, the lender will review the application and determine if the borrower meets the eligibility criteria. If the borrower is approved for the loan, they will need to attend a closing and sign the necessary paperwork to finalize the loan.

Final Thoughts

The USDA Rural Housing Mortgage Lender program is a great option for those who are looking to purchase a home in rural areas and meet the eligibility requirements. The program offers flexible credit requirements, low-interest rates, and no down payment required, making it an attractive option for low to moderate-income households.

While there are some drawbacks to the program, such as the restrictions on eligible areas and the requirement to pay mortgage insurance, these drawbacks may be outweighed by the benefits for some borrowers.

If you are considering the USDA Rural Housing Mortgage Lender program, it is important to do your research and determine if you meet the eligibility requirements. Once you have determined that you are eligible, you should consult with a lender who is approved to offer the program to learn more about the application process and to find out if the program is right for you.

If you are searching about Kentucky USDA Rural Housing Mortgage Lender: Difference Between 502 you've came to the right place. We have 7 Pictures about Kentucky USDA Rural Housing Mortgage Lender: Difference Between 502 like What is a USDA Loan? | PacRes Mortgage, Can You Put A Downpayment On A Usda Loan - Loan Walls and also El Paso County, Texas FHA, VA, and USDA Loan Information. Read more:

Kentucky USDA Rural Housing Mortgage Lender: Difference Between 502

kentuckyruralhousingusdaloan.blogspot.com loan usda direct guaranteed rhs down between difference guarantee kentucky money loans rural purchasing housing section program differences programs buying

USDA Loans | Connecticut Mortgage Broker | NimaLoans

www.nimaloans.com

www.nimaloans.com usda loans loan financing affordable

Can You Put A Downpayment On A Usda Loan - Loan Walls

loanwalls.blogspot.com

loanwalls.blogspot.com usda loan pros eligibility mortgages mortgagecalculator downpayment toploanmortgage rasheeda realtors nc qualify epik understanding payment

El Paso County, Texas FHA, VA, And USDA Loan Information

www.fedhomeloan.org

www.fedhomeloan.org fha

Can You Put A Downpayment On A Usda Loan - Loan Walls

loanwalls.blogspot.com

loanwalls.blogspot.com usda loans downpayment rural

USDA Loan Guidelines And Requirements | GOBankingRates

www.gobankingrates.com usda loans closing costs payment guide down gobankingrates guidelines excel db prev

What Is A USDA Loan? | PacRes Mortgage

pacresmortgage.com

pacresmortgage.com usda loan loans mortgage qualifying

Usda loans closing costs payment guide down gobankingrates guidelines excel db prev. Can you put a downpayment on a usda loan. Kentucky usda rural housing mortgage lender: difference between 502

{kind=link}

Post a Comment for "Usda Loan El Paso"